Bridge Loans: Understanding Their Role in Property Acquisition

Picture this: you’ve found your dream home, but there’s just one problem – you haven’t sold your current property yet. The seller wants a quick close, and traditional financing feels like it’s moving at a snail’s pace. This is where bridge loans come to the rescue, acting as a financial lifeline that can make or break your real estate dreams.

Bridge loans, also known as swing loans or gap financing, have become increasingly popular in today’s competitive real estate market. They’re designed to “bridge” the gap between buying a new property and selling an existing one, providing the quick access to capital that many property acquisitions demand.

Whether you’re a first-time homebuyer caught between properties or a seasoned investor looking to capitalize on time-sensitive opportunities, understanding bridge loans could be the key to unlocking your next real estate venture. Let’s dive deep into this powerful financing tool and explore how it might fit into your property acquisition strategy.

What Exactly Are Bridge Loans?

Bridge loans are short-term financing solutions typically lasting anywhere from a few weeks to 18 months, though most fall within the 6-12 month range. Think of them as the financial equivalent of a temporary bridge – they get you from point A to point B until a more permanent solution becomes available.

These loans are secured by real estate, often the property you’re purchasing or sometimes the one you’re selling. The beauty of bridge financing lies in its speed and flexibility. While traditional mortgages can take 30-45 days to close, bridge loans can often be arranged in as little as 7-14 days, making them invaluable in competitive markets where timing is everything.

The loan amounts typically range from $100,000 to several million dollars, with interest rates generally higher than conventional mortgages – usually ranging from 6% to 15%, depending on the lender and your financial profile. Yes, you’ll pay more for this convenience, but sometimes the opportunity cost of missing out on the perfect property far outweighs the additional interest expense.

How Bridge Loans Work in Property Acquisition

The mechanics of bridge loans are refreshingly straightforward. When you apply for bridge financing, lenders primarily focus on the value of the collateral property rather than your debt-to-income ratio or employment history – though these factors still matter to some degree.

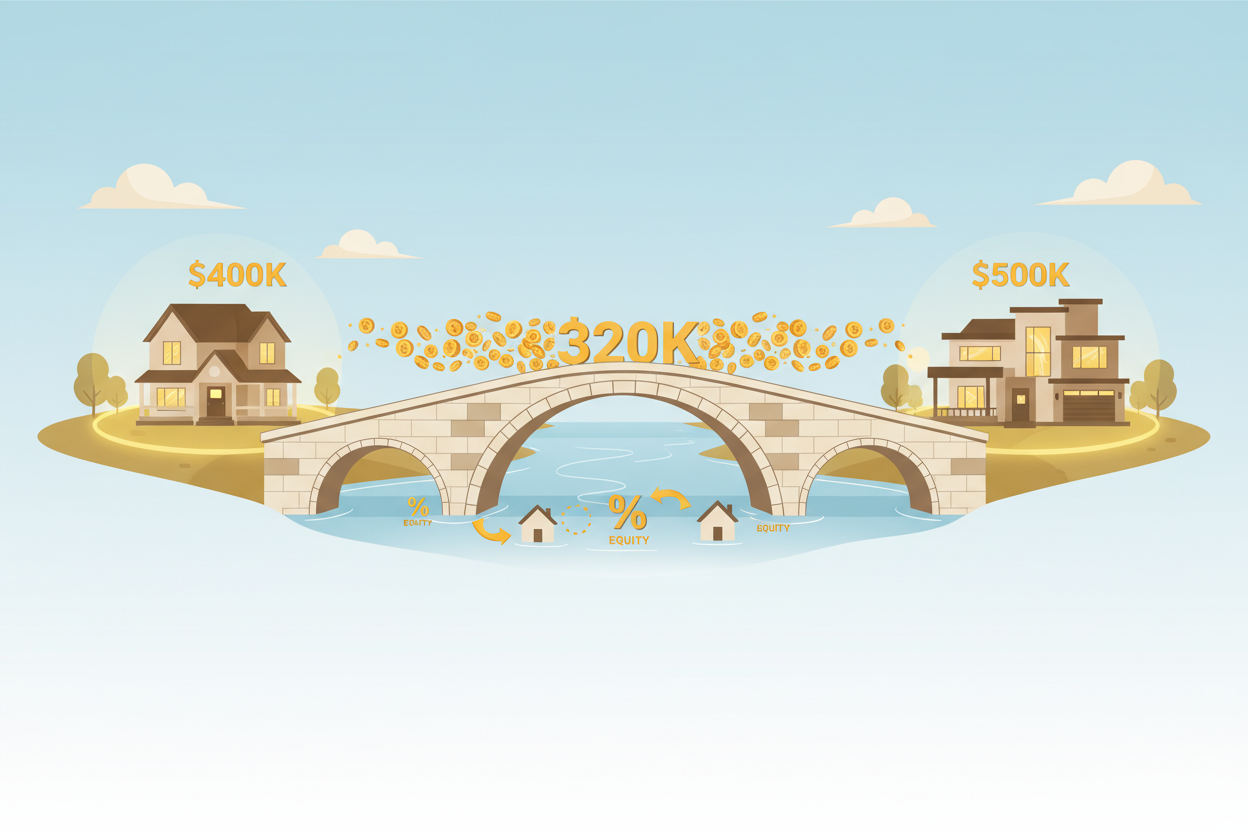

Here’s how a typical bridge loan scenario unfolds: Let’s say you own a home worth $400,000 with a $200,000 mortgage balance, giving you $200,000 in equity. You find a new home for $500,000 but haven’t sold your current property yet. A bridge lender might offer you a loan for up to 80% of your current home’s value, providing $320,000 in funding. This gives you enough to pay off your existing mortgage and have $120,000 toward your new home purchase.

The approval process moves quickly because bridge lenders rely heavily on the property’s appraised value and your equity position. They’re essentially betting on the real estate market and your ability to sell the existing property within the loan term. This asset-based approach allows for much faster underwriting than traditional mortgage loans.

When Bridge Loans Make Perfect Sense

Bridge loans aren’t for everyone, but they shine in specific situations. The most common scenario involves homeowners who need to purchase before selling their current property. In today’s market, where inventory is tight and good properties move fast, having the ability to make a non-contingent offer can be the difference between getting your dream home and watching it slip away.

Real estate investors also frequently use bridge loans to capitalize on time-sensitive opportunities. Whether it’s a foreclosure auction, a fix-and-flip project, or a commercial property that needs immediate attention, bridge financing allows investors to move quickly when conventional financing would take too long.

Another perfect use case is when you’re dealing with a chain reaction of property transactions. Maybe you’re selling one investment property to buy two others, or you’re upgrading your primary residence while simultaneously purchasing a vacation home. Bridge loans can help orchestrate these complex transactions without forcing you to time everything perfectly.

Construction and renovation projects also benefit from bridge financing. If you’re planning significant improvements to increase a property’s value before refinancing with a traditional mortgage, a bridge loan can provide the necessary capital to complete the work quickly.

The Advantages That Make Bridge Loans Attractive

Speed is undoubtedly the biggest advantage of bridge loans. In a world where real estate deals can fall through due to financing delays, having access to quick capital is invaluable. This speed advantage often translates into negotiating power – sellers prefer buyers who can close quickly and without financing contingencies.

Flexibility is another major benefit. Bridge loans often come with interest-only payment options, which can significantly reduce your monthly carrying costs during the transition period. Some lenders even allow you to defer payments entirely until you sell your existing property or secure permanent financing.

Bridge loans also provide breathing room in your decision-making process. Instead of feeling pressured to accept the first offer on your current home, you can afford to wait for the right buyer at the right price. This patience often results in better sale proceeds that more than offset the bridge loan costs.

For investors, bridge loans offer the ability to leverage opportunities that others might miss. Cash is king in real estate, and bridge financing essentially gives you cash-like purchasing power even when your capital is tied up in other properties.

Understanding the Risks and Drawbacks

While bridge loans can be incredibly useful, they’re not without risks. The most obvious concern is the higher cost of borrowing. Interest rates on bridge loans typically run 2-5 percentage points higher than conventional mortgages, and many come with additional fees including origination fees, appraisal costs, and sometimes prepayment penalties.

The short-term nature of these loans creates pressure to execute your exit strategy quickly. If your existing property doesn’t sell as expected or takes longer than anticipated, you might find yourself in a difficult financial position. Some borrowers end up extending their bridge loans at additional cost or, in worst-case scenarios, facing foreclosure if they can’t meet the repayment terms.

Market risk is another consideration. If property values decline during your bridge loan period, you might find yourself underwater on one or both properties. This scenario becomes particularly challenging if you need to sell at a loss to satisfy the bridge loan terms.

There’s also the stress factor to consider. Carrying two mortgage payments, even temporarily, can create significant financial and emotional pressure. Make sure you’re prepared for this reality before committing to bridge financing.

Qualifying for Bridge Loan Financing

Bridge loan qualification differs significantly from traditional mortgage underwriting. Lenders focus primarily on the loan-to-value ratio of the collateral property, typically allowing borrowing up to 70-80% of the property’s appraised value. Your credit score still matters, but it’s often less critical than with conventional loans – most lenders require a minimum score of 620-650.

Income verification is usually streamlined, though lenders want to see that you can handle the bridge loan payments along with any existing debt obligations. They’ll also want to understand your exit strategy – how and when you plan to repay the bridge loan.

Equity is crucial in bridge loan qualification. The more equity you have in your existing property, the more favorable terms you’re likely to receive. Some lenders also consider the equity you’ll have in the new property after purchase.

Documentation requirements are typically lighter than traditional mortgages, but you’ll still need recent tax returns, bank statements, and property information. The key difference is that this information is often reviewed and approved much more quickly than in conventional loan processes.

Alternatives to Consider

Before committing to a bridge loan, it’s worth exploring alternatives that might better suit your situation. Home equity lines of credit (HELOCs) can provide similar access to your property’s equity, often at lower interest rates, though they typically take longer to establish and may have lower borrowing limits.

Contingent offers represent another alternative, though they’re less attractive to sellers in competitive markets. A sale contingency allows you to make an offer on a new home contingent on selling your existing property, but many sellers will reject these offers in favor of non-contingent bids.

Some buyers opt for rent-back arrangements, where they sell their current home but negotiate to rent it back from the new owners for a few months while they complete their next purchase. This approach provides sale proceeds upfront while allowing time to find the right new property.

Hard money loans serve a similar function to bridge loans but typically come with even higher interest rates and shorter terms. They’re more common in investment scenarios and usually require significant real estate experience.

Making the Right Decision for Your Situation

Deciding whether a bridge loan makes sense for your property acquisition requires careful consideration of your financial situation, market conditions, and risk tolerance. Start by honestly assessing your ability to carry two mortgage payments and whether you have a realistic timeline for selling your existing property.

Consider the total cost of bridge financing, including interest, fees, and the opportunity cost of not having that capital available for other investments. Compare this cost to the potential benefits, such as securing your dream home or capitalizing on a time-sensitive investment opportunity.

Market conditions play a crucial role in this decision. In a hot seller’s market where properties move quickly, bridge loans might be essential for competitive offers. In a slower market, you might have more time to coordinate the sale of your existing property with your new purchase.

Your exit strategy should be rock-solid before proceeding with bridge financing. Have a realistic timeline for selling your property, and consider what you’ll do if the sale takes longer than expected. Some borrowers arrange backup financing or have additional resources available to extend the bridge loan if necessary.

Frequently Asked Questions

How quickly can I get approved for a bridge loan?

Bridge loans can typically be approved and funded within 7-14 days, though some lenders can move even faster in urgent situations. The key is having all your documentation ready and working with an experienced bridge lender who understands the time-sensitive nature of these transactions.

Can I get a bridge loan if I have bad credit?

While bridge lenders are more flexible than traditional mortgage lenders, credit still matters. Most require a minimum credit score of 620-650, though some may work with lower scores if you have substantial equity in your property. The interest rate and terms will likely be less favorable with poor credit.

What happens if I can’t sell my property before the bridge loan expires?

Most bridge loans offer extension options, though these come with additional fees and potentially higher interest rates. If you absolutely cannot repay the loan, the lender may foreclose on the collateral property. This is why having a solid exit strategy and backup plan is crucial.

Are bridge loans tax deductible?

The interest on bridge loans may be tax deductible, depending on how you use the funds and your specific tax situation. If you’re using the loan for investment property acquisition, the interest is typically deductible as a business expense. For personal residence purchases, the rules are more complex, so consult with a tax professional.

Can I use a bridge loan for commercial property acquisition?

Yes, bridge loans are commonly used for commercial real estate transactions. Commercial bridge loans often have higher loan amounts and may offer more flexible terms than residential bridge financing. The approval process focuses heavily on the property’s income potential and your experience as a commercial real estate investor.

Bridge loans represent a powerful tool in the property acquisition toolkit, offering speed and flexibility when timing is critical. While they come with higher costs and inherent risks, they can make the difference between securing your ideal property and watching it slip away. The key is understanding when they make sense for your situation and ensuring you have a solid plan for repayment. With proper planning and realistic expectations, bridge loans can successfully bridge the gap between where you are and where you want to be in your real estate journey.

Free Stuff!

Add CTA sections description.