Mezzanine Financing: How It Works and Why It Matters

Picture this: you’re a business owner with ambitious growth plans, but traditional bank loans feel too restrictive, and giving up equity to venture capitalists seems premature. Enter mezzanine financing – the financial world’s equivalent of having your cake and eating it too. This hybrid funding solution has become increasingly popular among companies seeking flexible capital for expansion, acquisitions, or strategic initiatives.

Mezzanine financing represents a sophisticated middle ground between debt and equity financing, offering unique advantages that make it an attractive option for both growing companies and savvy investors. Whether you’re an entrepreneur exploring funding options or an investor seeking higher returns, understanding mezzanine financing could be the key to unlocking new opportunities in today’s competitive business landscape.

What Is Mezzanine Financing?

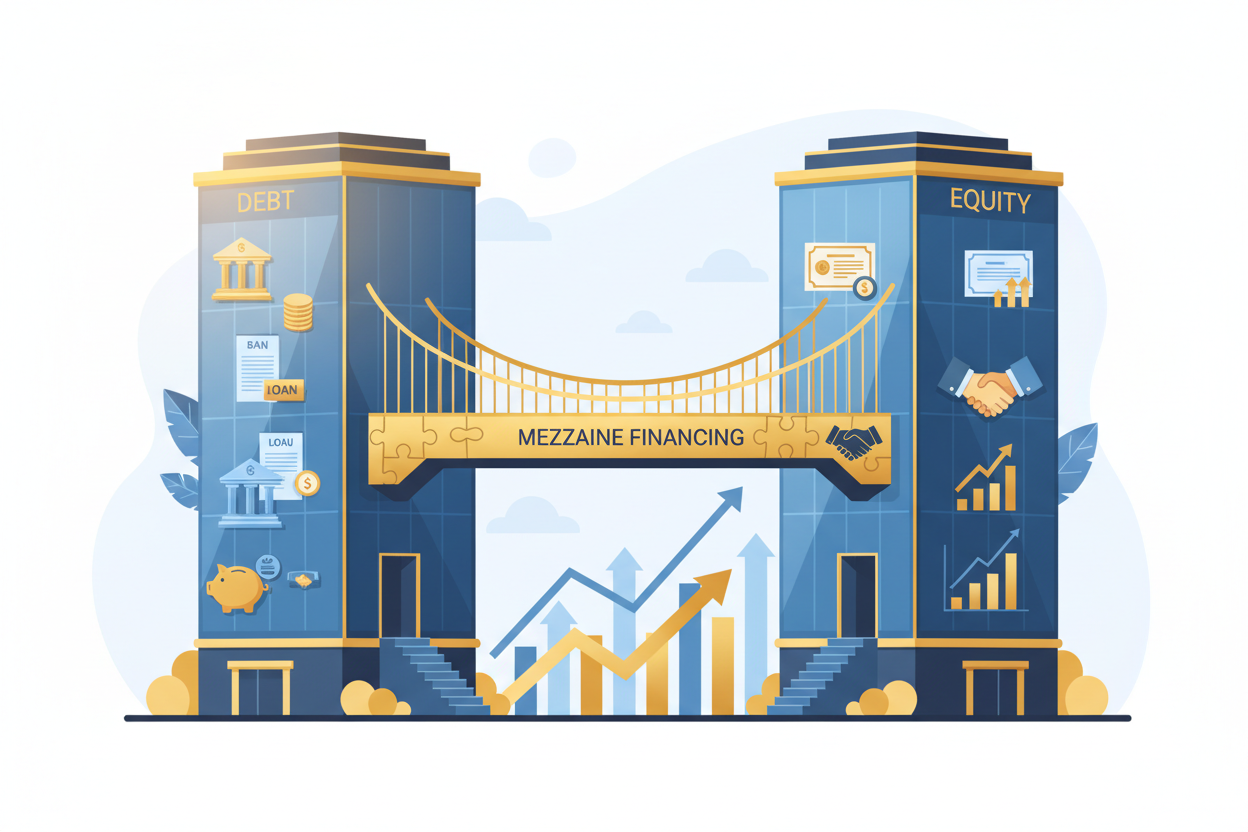

Mezzanine financing is a hybrid form of capital that combines elements of debt and equity financing. Think of it as a financial bridge that connects traditional loans with equity investments. This structure typically involves subordinated debt or preferred equity that gives lenders the right to convert their investment into ownership stakes if certain conditions aren’t met.

The term “mezzanine” comes from architecture, referring to the intermediate floor between main floors of a building. Similarly, mezzanine financing sits between senior debt (like bank loans) and equity financing in a company’s capital structure. This positioning makes it more expensive than traditional debt but less dilutive than pure equity financing.

What makes mezzanine financing particularly interesting is its flexibility. Lenders often receive both interest payments and equity kickers – such as warrants or conversion rights – that provide additional upside potential. This dual benefit structure explains why mezzanine financing has become a go-to solution for companies in transition phases or those pursuing aggressive growth strategies.

How Mezzanine Financing Works

The mechanics of mezzanine financing involve several key components that distinguish it from traditional funding methods. At its core, mezzanine capital is structured as subordinated debt, meaning it ranks below senior debt but above equity in the event of liquidation or bankruptcy.

Typically, mezzanine financing carries interest rates ranging from 12% to 20%, significantly higher than traditional bank loans but justified by the increased risk and potential returns. The payment structure often includes both current interest payments and payment-in-kind (PIK) interest, which compounds over time rather than being paid immediately.

The equity component usually comes in the form of warrants or conversion features. These give mezzanine investors the right to purchase equity at predetermined prices or convert their debt into ownership stakes. This structure allows investors to participate in the company’s growth while providing downside protection through the debt component.

The timeline for mezzanine financing typically ranges from three to seven years, with many deals structured around five-year terms. During this period, companies usually make interest-only payments, with the principal due at maturity. This payment structure helps preserve cash flow for growth initiatives while the business scales.

Types of Mezzanine Financing

Mezzanine financing isn’t a one-size-fits-all solution. Several variations exist to meet different business needs and investor preferences. Understanding these types helps companies choose the most appropriate structure for their specific circumstances.

Subordinated debt represents the most common form of mezzanine financing. This structure involves loans that rank below senior debt but include equity kickers like warrants. Companies benefit from interest deductibility while investors gain potential upside through equity participation.

Preferred equity mezzanine financing provides investors with preferred stock that pays dividends and includes conversion rights. This structure often appeals to companies wanting to avoid additional debt on their balance sheets while still accessing growth capital.

Convertible securities offer another popular variation, allowing investors to convert their holdings into common stock under specific conditions. This flexibility benefits both parties – companies maintain debt treatment for tax purposes while investors position themselves for equity gains.

Revenue-based mezzanine financing has gained traction recently, particularly among technology and service companies. Instead of traditional interest payments, investors receive a percentage of company revenues until they achieve predetermined returns.

Benefits for Companies

Companies choose mezzanine financing for compelling reasons that extend beyond simple capital access. The flexibility inherent in mezzanine structures often makes them more attractive than traditional alternatives, especially for businesses in growth phases or transition periods.

One primary advantage is preservation of ownership control. Unlike equity financing, which immediately dilutes existing shareholders, mezzanine financing allows founders and management teams to maintain operational control while accessing significant capital. The equity component typically only activates under specific circumstances or at the investor’s discretion.

Cash flow management represents another significant benefit. Mezzanine financing often features interest-only payments or payment-in-kind structures that preserve working capital for growth initiatives. This flexibility proves invaluable for companies investing heavily in expansion, research and development, or market penetration strategies.

The subordinated nature of mezzanine debt also provides balance sheet advantages. While more expensive than senior debt, mezzanine financing doesn’t typically require the same level of collateral or restrictive covenants found in traditional bank loans. This freedom allows companies to operate more independently while pursuing strategic objectives.

Tax benefits add another layer of attractiveness. Interest payments on mezzanine debt remain tax-deductible, reducing the effective cost of capital compared to equity financing. This advantage can significantly impact overall financing costs, especially for profitable companies in higher tax brackets.

Benefits for Investors

From an investor perspective, mezzanine financing offers an attractive risk-return profile that bridges the gap between conservative debt investments and high-risk equity positions. This positioning appeals to institutional investors seeking steady income with upside potential.

Higher returns represent the most obvious investor benefit. Mezzanine investments typically target returns in the 15-25% range, significantly exceeding traditional debt investments while providing more predictable income than pure equity plays. This return profile attracts pension funds, insurance companies, and other institutional investors with specific yield requirements.

The hybrid structure provides multiple exit strategies and return mechanisms. Investors receive regular interest payments for steady income while maintaining options to participate in company growth through equity features. This dual-income approach reduces overall investment risk while preserving upside potential.

Priority in liquidation scenarios offers additional protection. While subordinated to senior debt, mezzanine investors rank ahead of equity holders in bankruptcy or liquidation proceedings. This positioning provides downside protection that pure equity investments lack.

Portfolio diversification benefits make mezzanine financing attractive to sophisticated investors. The asset class typically exhibits lower correlation with public markets while providing exposure to middle-market companies that might otherwise be inaccessible to institutional investors.

Common Use Cases

Mezzanine financing serves various strategic purposes, making it valuable across different business scenarios and industry sectors. Understanding these applications helps companies identify when mezzanine capital might be the optimal funding solution.

Growth capital represents the most common application for mezzanine financing. Companies with proven business models seeking to expand operations, enter new markets, or launch new products often find mezzanine capital ideal for funding these initiatives without surrendering significant equity or accepting restrictive debt covenants.

Management buyouts frequently utilize mezzanine financing to bridge funding gaps. When management teams acquire companies from private equity firms or corporate parents, mezzanine capital often provides the additional leverage needed to complete transactions while maintaining reasonable equity contributions.

Acquisition financing represents another popular use case. Companies pursuing strategic acquisitions often employ mezzanine financing to supplement senior debt and equity contributions. This approach allows acquirers to complete larger transactions while preserving cash for integration and operational improvements.

Recapitalization scenarios also benefit from mezzanine structures. Existing shareholders seeking partial liquidity without selling control often use mezzanine financing to fund dividend recapitalizations or facilitate partial ownership transfers.

Risks and Considerations

While mezzanine financing offers compelling advantages, companies must carefully consider associated risks and potential drawbacks. Understanding these factors ensures informed decision-making and appropriate structure selection.

Higher cost of capital represents the most immediate consideration. Mezzanine financing typically costs significantly more than traditional debt, potentially impacting profitability and cash flow. Companies must ensure that growth initiatives or strategic benefits justify these increased financing costs.

Potential dilution through equity features requires careful evaluation. While immediate dilution may be limited, conversion rights and warrants can significantly impact ownership percentages if activated. Companies should model various scenarios to understand potential dilution implications.

Complexity in structure and documentation often exceeds traditional financing arrangements. Mezzanine deals typically involve sophisticated legal documentation, multiple stakeholder interests, and ongoing compliance requirements that can burden management teams and increase administrative costs.

Limited control over timing presents another challenge. Mezzanine investors may have rights to force liquidity events or influence strategic decisions, particularly if companies fail to meet performance targets or financial covenants. This potential loss of autonomy requires careful consideration during structure negotiations.

The Future of Mezzanine Financing

The mezzanine financing market continues evolving as economic conditions, regulatory changes, and investor preferences shape industry dynamics. Several trends suggest continued growth and innovation in this financing sector.

Technology integration is transforming how mezzanine deals are sourced, evaluated, and managed. Digital platforms now connect companies with mezzanine investors more efficiently, while data analytics improve risk assessment and pricing accuracy. These technological advances are making mezzanine financing more accessible to smaller companies and regional markets.

ESG considerations are increasingly influencing mezzanine investment decisions. Investors are incorporating environmental, social, and governance factors into their evaluation processes, potentially favoring companies with strong sustainability profiles or positive social impact.

Market expansion into new sectors continues as mezzanine investors seek opportunities beyond traditional industries. Healthcare, technology, and renewable energy sectors are attracting increased mezzanine capital as investors pursue growth in dynamic markets.

Regulatory changes may impact mezzanine financing structures and availability. Banking regulations, tax policy modifications, and capital requirements for institutional investors could influence how mezzanine financing is structured and priced in future markets.

Frequently Asked Questions

What is the typical size range for mezzanine financing deals?

Mezzanine financing deals typically range from $5 million to $100 million, though larger transactions exceeding $500 million occur in major corporate situations. The sweet spot for most mezzanine funds is between $10 million and $50 million, targeting middle-market companies with established operations and growth potential.

How does mezzanine financing differ from venture capital?

Mezzanine financing focuses on established companies with proven revenue streams and cash flow, while venture capital typically targets early-stage companies with high growth potential but limited operating history. Mezzanine investments provide more predictable returns through debt-like structures, whereas venture capital seeks higher returns through pure equity appreciation.

Can companies refinance mezzanine debt early?

Yes, most mezzanine financing agreements include prepayment provisions, though early refinancing often involves prepayment penalties or make-whole provisions. Companies should negotiate these terms carefully during initial structuring to maintain flexibility for future refinancing opportunities.

What financial metrics do mezzanine lenders typically require?

Mezzanine lenders generally require minimum EBITDA of $3-5 million, debt service coverage ratios above 1.2x, and demonstrated cash flow stability. They also evaluate management team experience, market position, and growth prospects when making investment decisions.

How long does the mezzanine financing process typically take?

The mezzanine financing process usually takes 60-90 days from initial contact to closing, depending on deal complexity and due diligence requirements. This timeline includes term sheet negotiation, due diligence, legal documentation, and final approvals. Simple transactions may close faster, while complex deals could take longer.

What happens to mezzanine investors when companies go public?

When companies go public, mezzanine investors typically convert their debt into equity or receive cash repayment from IPO proceeds. The specific outcome depends on deal structure and conversion terms negotiated during initial financing. Many mezzanine agreements include provisions for liquidity events like public offerings.

Free Stuff!

Add CTA sections description.